“The number one bank in the world will be a technology company,” Fintech influencer, author and futurist Brett King once said. 2020 drove home the truth on this statement. While there have several triggers over the years—from demonetization to digital innovations—, nothing amplified the need to embrace digital banking more than the pandemic that we are all recovering from. For the skeptics seeking numbers, 42% of Indians used digital payment multiple times as compared to the pre-lockdown period. The same trends were reflected globally as well. There was a 72% increase in the use of financial apps and mobile banking services in Europe.

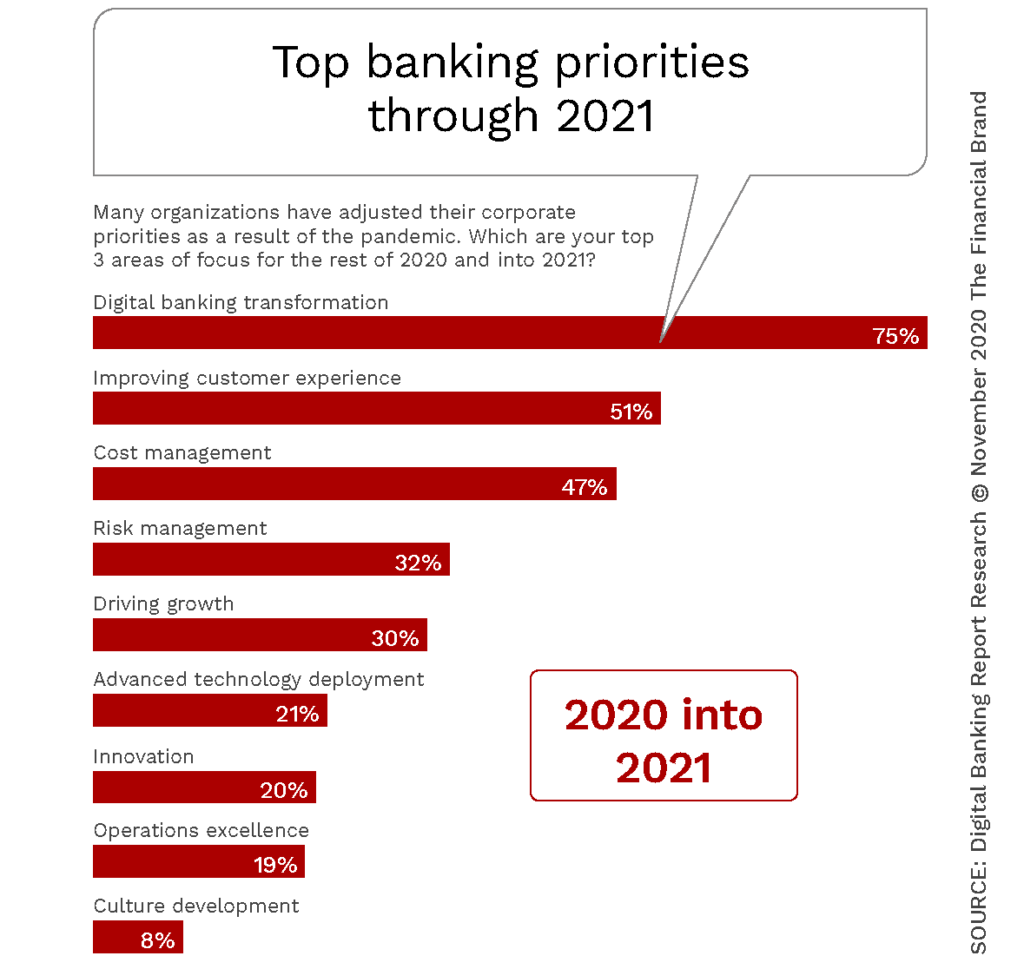

As banking and financial institutions, the world over is formulating their bounce-back strategies, digital is all set to feature in a predominant role of shaping the existing and evolving customer experience (CX). As per the Digital Banking Report, the top strategic priorities of global finance companies for this year and beyond are digital banking transformation and improving customer experience.

source: Top 7 Customer Experience Trends in Banking

However, most vital to remember is that while the pandemic brought on the migration to digital banking services, it will be up to the superior CX you offer that will keep your customers coming back for more. Driving digital CX strategies will be foundational to bounce back, transform and succeed in the new post-COVID paradigm.

Just knowing who your consumers are will not suffice anymore. The new normal calls for proactive personalization. Consumers now want banks to manage their finances just like a GPS manages your journey to your final destination. Driven by Artificial Intelligence (AI), open banking and account aggregation, personalization can be leveraged to align real-time transaction insights with the bank’s products and services. From personalized financial insights and reminders of financial activity such as shifting excess funds into saving for retail customers to providing SMBs with a single source of truth through integrations—banks can augment the CX journey with custom insights. What’s more! It’s beneficial to banks too! Boston Consulting Group (BCG) estimated that large-scale successful implementation of personalization could increase a bank’s annual revenue by 10%.

Another razor-sharp customer experience strategy for 2021 is ensuring channel uniformity through omnichannel banking. The customer today interacts with banks through different touchpoints. These touchpoints change frequently depending upon where a customer is and what they might be doing. They may choose to carry out a transaction physically at the branch, or online using a mobile or laptop, with the help of a call center representative or even through a voice-command device. Irrespective of the option your customer selects they expect to have identical experiences each time. A true omnichannel CX strategy should enable customers to seamlessly switch from one channel to another without the bank losing track of their journey. With 2021 amplifying digital touchpoints, banks need to stay one step ahead by facilitating this expectation of uniformity of the buying and contact experience.

When we look to defining a customer comfort criteria set, digital simplicity, UX, data and system security and speed of engagement are vital to driving trust, loyalty and retention. Engagement tools like Personal Finance Management (PFM) and Multi-bank PFM, Prepaid Banking platforms and Digital Onboarding while contributing to building the CX experience will gain adoption only when the desired levels of customer comfort are met.

The success of CX strategies in 2021 will also depend on financial brands building an experience-driven ecosystem. The brand perception today largely depends on the digital presence. App ratings on Google Play and the App Store; reviews and feedback on social media platforms, forums and other sites; net promoter score (NPS) – how likely customers are to recommend your banking product; customer lifetime value (CLV)—all contribute to building and defining the CX journey.

In conclusion, it’s important to reiterate that while the pandemic acted as a catalyst, much higher expectations lie ahead. EY’s August 2020 Future Consumer Index, which analyzed consumer behavior in banking and financial services, found that only 24% of survey respondents were positive that banks would operate more digitally in the next one to two years. This indicates that you can’t just assume that customers will remain digitally involved. Enhancing the overall CX journey for your retail and corporate customers, by making it as frictionless as possible, is what will help catapult your post-COVID digital strategies.