Mobile banking: a new dawn for Bangladesh

Over the past few years, Bangladesh’s banking sector has seen great transformation. The advent of mobile banking has sparked a revolution, challenging traditions and presenting innovative opportunities. As of December 2022, the number of internet banking customers has crossed 6.2 million, marking a 40.83% increase compared to the previous year. This surge can be attributed to many factors.

Here’s a look at Bangladesh’s global perspective and how banks can target the new wave of customers in this ever-changing landscape.

Where does Bangladesh stand in the global perspective?

Bangladesh’s surge in mobile money adoption is part of a much bigger wave sweeping across the globe, particularly visible in the South and Southeast Asian regions. This trend points to a universal truth: a mix of supportive ecosystems, smart regulations, and strategic collaborations can drive financial inclusion. Countries leading in this domain showcase how effectively leveraging these elements can open up financial services to wider segments of the population, including the previously unbanked or underbanked.

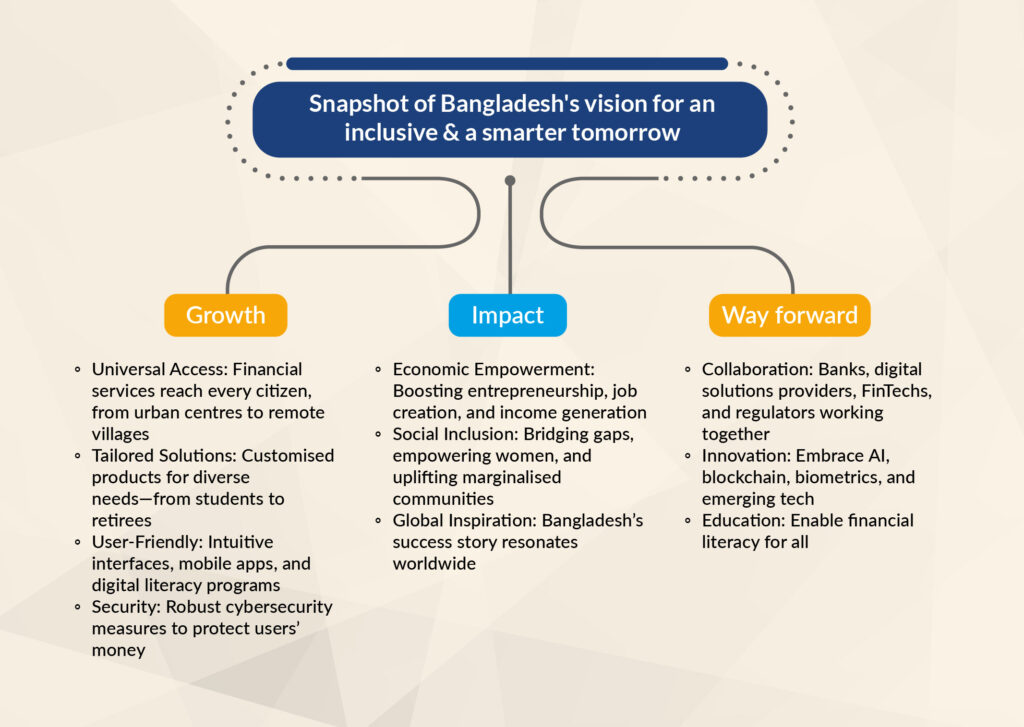

In response to this global movement, Bangladesh has crafted the National Financial Inclusion Strategy (NFIS) for the period of 2021 to 2026. This ambitious strategy is designed to broaden the access, usage, and overall quality of financial services across all demographics.

At the heart of this strategic push is Digital Financial Services (DFS), with a special emphasis on Mobile Financial Services (MFS). By capitalising on the widespread adoption and convenience of mobile technology, Bangladesh aims to enhance its citizens’ financial well-being and catalyse economic growth and development.