Yes! Understanding that a customer goes through various stages helps, but examining what they go through on a psychological level provides many insights that can propel a business’s digital transformation.

But first, here’s a quick introduction to what is and why:

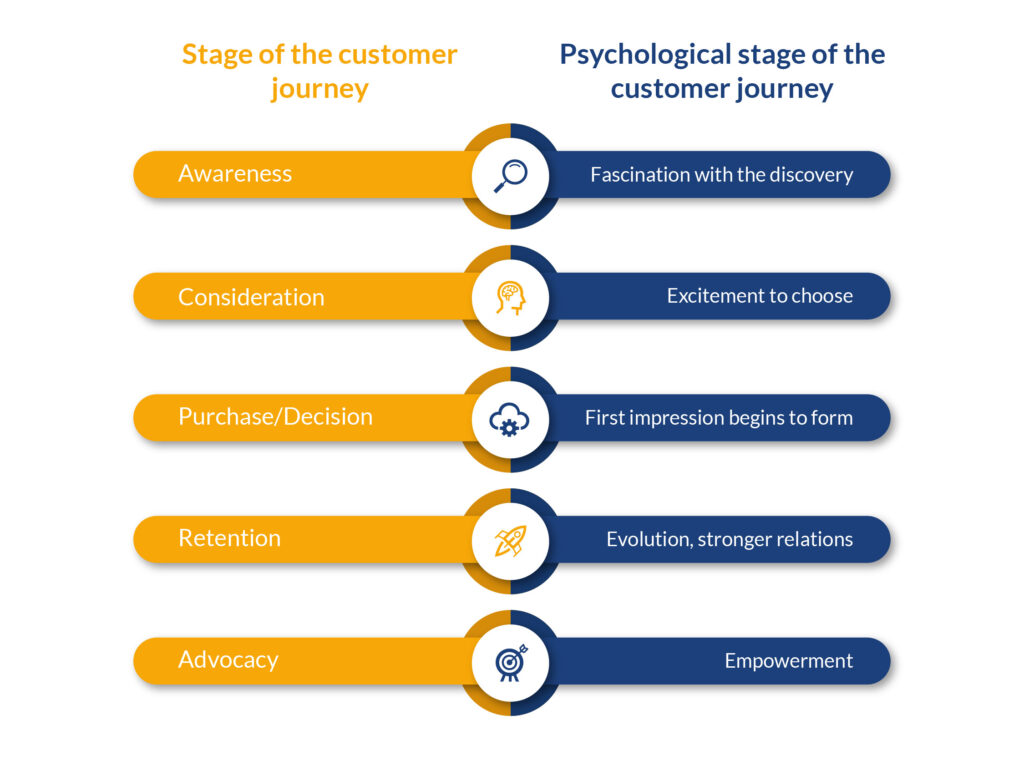

A business understands that a customer’s journey is conveniently divided into five stages amongst the presales, sales, and post-sales categories.

Awareness stage, where the customer is expected to learn that they have a need. Then comes the consideration stage, where they seek solutions and weigh their options. The decision happens in the next stage, soon after which businesses go through a lull in their pace—the retention stage. After which comes the advocacy stage where brand loyalty is established.

However, customers are people too. And there can never be an accurate prediction of what each one of them is thinking at a given point in time. Which is why learning how these stages impact one’s mind matters too.

Understanding the nuanced psychological states of customers at each phase of their banking journey is the key to creating a customer-centric strategy that truly resonates, so let’s try to map out what that would look like.

In the awareness stage, when the customers are fascinated and are discovering and exploring, there are a lot of options they are looking at. Their attention is short, and convenience in their digital banking experience is what they seek. This is interestingly a reflection on why people slowly reduced frequenting a bank. “Consumer visits to retail bank branches are set to drop 36% between 2017 and 2022, with mobile transactions rising 121% in the same period,” Financial brand.

What a bank must aim to achieve here is showcasing their solutions the most. Usually, having convenient, reliable, and seamless digital banking solutions helps!

The consideration stage can either overwhelm the customers or excite them into making the final decision. Customers carefully weigh their options. A bank can have the most lucrative offerings and recommendations for their needs, but if it doesn’t provide them with enough evidence, chances are, customers leave!

Here, the bank should focus on delivering value propositions, showcasing competitive advantages, and guiding potential customers through the decision-making process.

Once the customer decides to invest in a bank’s offering, the real challenge begins. As a customer engages with the banking platform, they are constantly evaluating and assessing their decision. This is why customer onboarding has been the most tricky process. Customers realise that ease of usage and the promise of a seamless experience is not very common after all.

To propel the customer forward, banks must aim to automate long processes, offer seamless CX journeys, and provide a jargon-free banking experience.

In the retention stage, a customer is familiar with the bank’s digital banking platform and is either a satisfied customer or a customer looking to switch. Either way, no customer sticks in one stage for too long, and banks must aim at improving their offerings and meeting their customers’ needs.

The advocacy stage presents a near-utopian opportunity for banks! The focus should be on empowering customers by actively promoting referral programs, testimonials, and incentives. This not only cultivates positive word-of-mouth but also improves the bank’s adoption rate. The advocacy stage is all about the repeated use of the banking application to foster loyalty to ensure higher return on investment (ROI).

How to utilise this piece of information?

That’s quite simple.

Understanding what customers feel and go through can be vast, and we might never fully get it. But this can be a launchpad for banks to get going. Your customer is your next-door neighbour, your daughter’s teacher, or even yourself!

Are you the bank that you would want to bank with?