The pandemic-induced digital transformation has upended business-as-usual. As a result, the banking sector has had to rethink its services, core structures, and how it interacts with its customers.

Impact of Covid on Retail Banking

Here are some of the ways Covid has changed retail banking. While many of these changes have permanently changed how banks operate, it remains to be seen what remains once Covid is over, and operations return to normal.

- Risk-averse consumers impacting revenue streams: With lost jobs and many consumers struggling to make ends meet after two years of lockdowns, delinquencies and missed payments are on the rise. In Canada, it is estimated that loan defaulters have increased by 50-70%3. In addition, consumers have lost their risk appetite with many bolstering their savings and liquid cash reserves. This will eat into the already meagre margins that banks were making on loans and will cause banks to look at tightening their expenses to tide over.

- Deep internal cost reductions and restructuring in alignment with changing long-term vision: With teams working remotely for the most part of the last few years, banks have evolved to a higher level of efficiency. And technology has enabled it. Some processes, previously performed by people, have been digitized while technology projects that were on the backburner have been accelerated to cope with the virtual banking demands during the pandemic. Banks have become leaner and more profitable enabled by these technology enhancements.

- Changing rules and regulations to aid recovery: Governments, the world over, have partnered with banks to aid in the rescue and recovery of businesses and individual wealth during the pandemic. From the South Korean government distributing consumption coupons for low-income households, CBILS in the UK, Cura Italia in Italy and the CARES Act in the US, policies and regulations are being changed to align with bolstering the economy. And the banking sector has had to step up and aid these conversations. Banks, today, work with corporates and commercial real estate managers to ensure a safe return-to-work passage in keeping with government-issued rules and regulations. Banks will continue to be called upon to work with governments to play a societal role beyond their traditional role in the future as well.

- Increased digital adoption and changing customer banking habits: Direct sales, self-service, digital advice, virtual banking, and digital payments have all seen an accelerated adoption during the pandemic. Even the fence-sitters, who were reluctant to trust digital banking, have had to embrace it out of necessity. This new-found comfort with technology will hasten the digitization of banking processes that normally would have taken years. This will lead to banks restructuring their internal teams while they focus on enabling their customers through automation and digital platforms.

Key Drivers of Change

From lockdowns and restricted movement to currency notes being seen as potential Covid virus carriers, retail banking was stripped bare to its most basic functions during the pandemic. When, however, even mundane activities like grocery shopping went online, banking was not far behind. To give you an idea of the growth of digital banking during the pandemic, consider these numbers from the Bank of America. The world’s-leading bank added more than 2 million active digital clients in 2021, a single-year record, taking its total number of verified digital users to more than 54 million, with a record 10.5 billion virtual log ins, in 20204.

While it remains to be seen whether customers return to pre-covid behaviour once the pandemic ends, the following factors continue to drive the need for digitisation in the banking sector.

- The growing threat of Fintech – Technology giants and startups alike have turned their focus to the banking industry. From creating ecosystems that include mobile payment wallets to super apps that interface with banking software on the backend, fintechs are commanding a higher share of the market. In order for the banking sector to remain relevant, it needs to move into the future.

- Changing business models: Lockdowns and rising costs have resulted in shrinking margins across the banking industry. Yet, digital-only players continue to thrive, experiencing a revenue growth of 70% higher than traditional banks. Banks need to transition from traditional linear business models to non-standard productised business models that cater exclusively to customers’ requirements.

- Evolving customer requirements: With convenience and personalised options being the lynchpin upon which purchase decisions are made in every other sphere of their lives, customers—especially digitally-savvy millennials and Gen-Zers—expect banks to deliver the same, superior experiences. According to an Insider Intelligence report, 45% of the survey’s respondents identify mobile features as the top-three factors that help determine which bank to use5. And if customers can’t find what they need, 40% say they will switch to a competitor6.

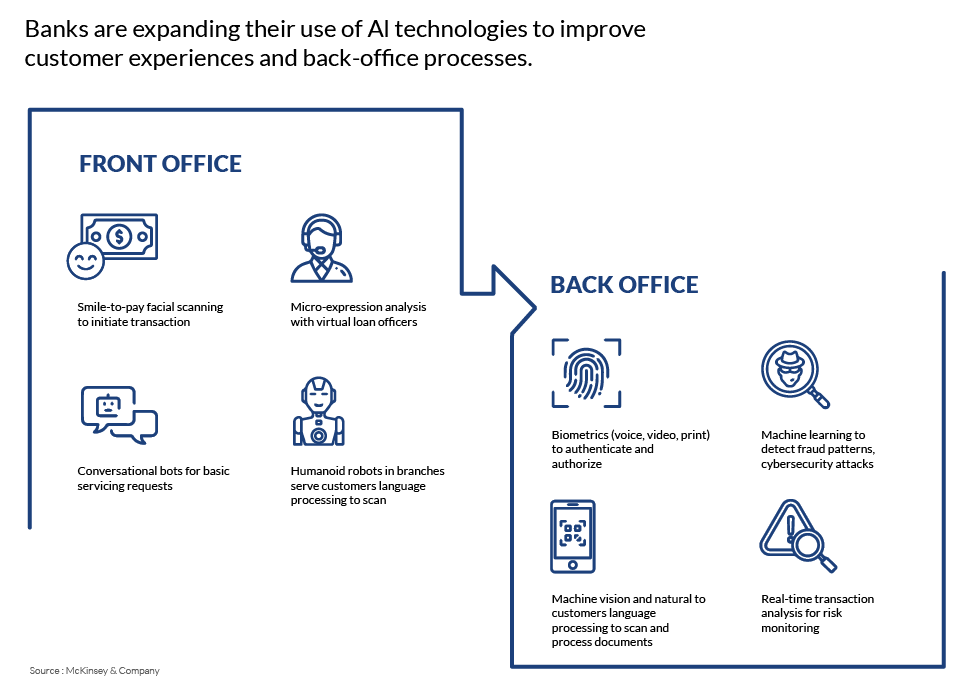

AI-powered digitisation, an emerging differentiator

As banks continue to compete for a customer’s attention in an increasingly crowded and noisy environment, many ‘first movers’ have found a key differentiator—using artificial intelligence (AI) and machine learning (ML) to attract customers and deliver superior experiences.

Consider the use case of Erica®, the Bank of America’s AI-driven virtual financial assistant launched in 2018. Since then, customers have interacted with Erica® over 659 million times for 230 million requests. In 2021, customer interactions with Erica were nearly twice the total of the previous two and a half years, with 123 million interactions taking place in Q4 2021 alone, a 247% year-over-year increase. Nearly 7 million clients engaged with Erica for the first time, and interactions among wealth management clients increased by 418% year-over-year7. By creating an effortless way for customers to interact with them, Bank of America has delivered on the promise of superior customer experiences, even earning the award for the “Best Consumer Digital Bank in the U.S.” by Global Finance in 2020.

McKinsey estimates that AI technologies could potentially deliver up to $1 trillion of additional value each year for the banking sector8. According to the report, AI technologies can help boost revenues through increased personalisation of services to customers, lower costs through efficiencies generated through automation and reduced errors rates, and uncover unrealised opportunities by parsing vast amounts of data.