In this blog, we delve into understanding the drivers of digital transformation in rural Bangladesh and explore where it is headed.

How is digital banking sparking rural economic empowerment?

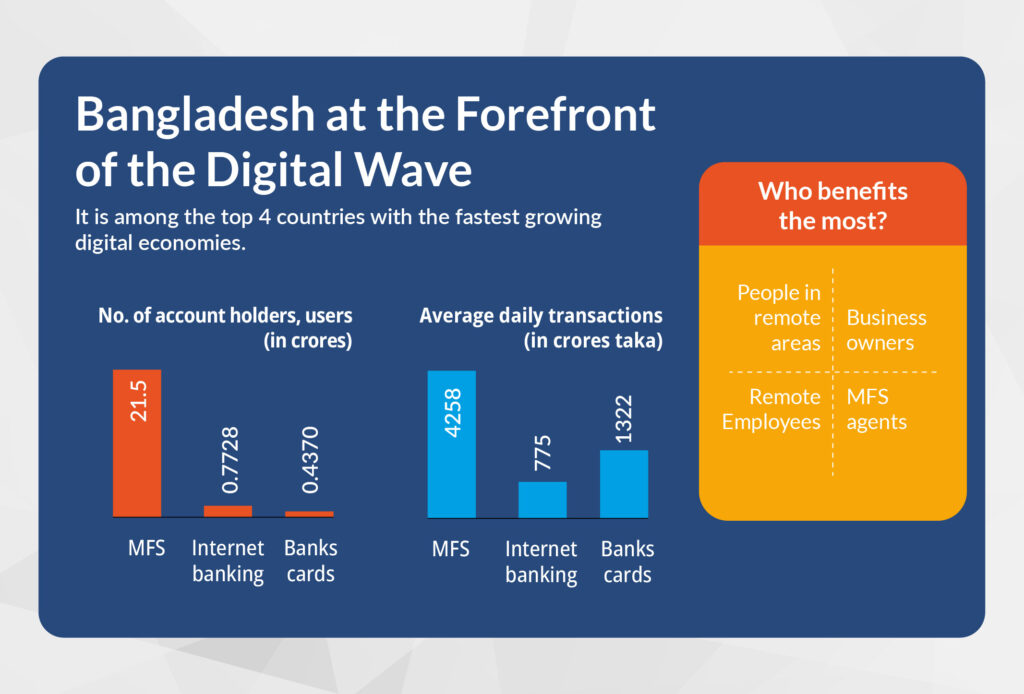

Bangladesh has been actively pursuing socio-economic development initiatives for some time now. By enabling mobile banking, Bangladesh has opened a whole new world of opportunities to the people living in remote regions of Bangladesh.

According to a report by the World Bank, the adoption of digital banking in Bangladesh has led to an increase in rural economic activities. The report states that digital banking has enabled rural households to access formal financial services, which has led to an increase in savings and investments. The report also highlights that digital banking has enabled rural households to access credit, leading to increased entrepreneurship and market access.

Technological innovations driving financial inclusion in Bangladesh

In Bangladesh, digital banking in rural banking blends convenience with innovation, placing innovation within arms reach. Bangladesh relied on the following innovative solutions to make digital banking a reality for the remote regions.

- USSD Utilisation: Employs Unstructured Supplementary Service Data (USSD) for mobile banking without internet, crucial in low-connectivity regions.

- Agency Banking and AEPS: Expands banking reach through agency banking and Aadhaar Enabled Payment System (AEPS) for seamless transactions.

- AI and Machine Learning Integration: Enhances customer service, fraud detection, and risk assessment through artificial intelligence and machine learning.

- Robo-Advisors: Offers automated investment advice, gaining popularity among users.

- Chatbots and Virtual Assistants: Improves customer support with AI-driven chatbots and virtual assistants, providing immediate assistance.

In addition, Open banking has enabled banks to expand their reach in rural areas through partnerships with mobile financial service providers. For example, bKash and Nagad, two mobile financial service providers in Bangladesh, have integrated open banking into their platforms and partnered with banks to provide customers with access to their bank accounts through their apps.

This has made banking more accessible and convenient for people living in remote areas.

Where is it headed?

The future of digital banking in rural Bangladesh is promising. The country aims to make 75% of local transactions digital by 2027 as part of its vision of a “Smart Bangladesh” by 2041. Digital banking has already seen exponential growth in rural areas, with fully online banking branches witnessing a compound annual growth rate of 6.8% from 2019 to 2023.

Clayfin is a leading provider of digital banking solutions that can help traditional banks with their digital transformation in rural Bangladesh. Our omnichannel banking experience platform is designed to provide a superior digital customer experience strategy. We offer the right value ingredients for banks to establish an enriched customer experience.

We have worked with many banks worldwide, including BRAC bank of Bangladesh, offering innovative and personalised digital banking solutions. Our collaboration with BRAC enabled them to introduce ‘Astha’, a mobile application and internet banking portal. The app gained popularity as the leading banking app for offering user-friendly features. With our expertise, they benefited from:

- 30% customer growth in less than a year

- 100% growth in digital transaction numbers and volumes

- 36% shift from manual transactions to digital channels

- Aastha facilitated transactions totaling up to 5000 crore TK

Looking to achieve similar results? Get in touch with our experts today.