In the global shift towards a cashless society, Bangladesh is carving out its unique path, supported by a tech-savvy population and a fast-growing economy. With mobile financial services (MFS) transactions surging fourfold to over Tk 4,100 crore in the past five years, the adoption of digital payments is steadily gaining momentum.

Backed by a proactive government and a banking system eager to innovate, the journey towards a cashless economy in Bangladesh is not just an opportunity for transformation but also a test of resilience against its unique challenges.

The Momentum Behind the Shift

Bangladesh’s journey towards a cashless economy has been catalysed by multiple factors. Mobile financial services (MFS) have become a cornerstone of financial inclusion.

Platforms like bKash and Nagad have revolutionised the way people transact, offering easy access to digital payments even in remote areas. For instance, bKash, with over 65 million users, processes millions of transactions daily, demonstrating the appetite for cashless solutions.

Additionally, the government has rolled out policies to encourage digital adoption. Initiatives such as the Digital Bangladesh Vision 2021 aim to create an ecosystem where cashless transactions thrive. From digitising utility bill payments to introducing QR-based payment systems in retail, the groundwork is being laid for a transformative financial landscape.

Plenty of Opportunities Ahead

Bangladesh stands on the brink of transformative benefits as it moves towards a cashless society.

- Financial Inclusion:

Digital banking solutions are reshaping access to financial services, particularly for the unbanked. With over 190 million mobile phone users, mobile wallets and banking apps are driving accessibility and empowering underserved populations.

- Economic Growth and Efficiency:

Transitioning away from cash reduces the inefficiencies tied to physical currency management. Transparent digital payment trails not only enhance tax compliance but also contribute to building a more robust and accountable financial ecosystem.

Addressing the Roadblocks

While the opportunities are vast, significant hurdles must be addressed for Bangladesh to fully embrace a cashless economy.

- Infrastructure and Accessibility Gaps:

Many areas in Bangladesh still struggle with outdated banking systems and unreliable internet connectivity. Bridging this digital divide is essential to ensuring that rural populations are not left behind.

- Trust and Regulatory Framework:

Concerns over data privacy and cybersecurity continue to discourage some users from adopting digital payment methods. Additionally, the regulatory framework needs to be strengthened to address issues like interoperability and anti-money laundering.

Addressing these challenges is key to unlocking the full potential of a cashless society in Bangladesh.

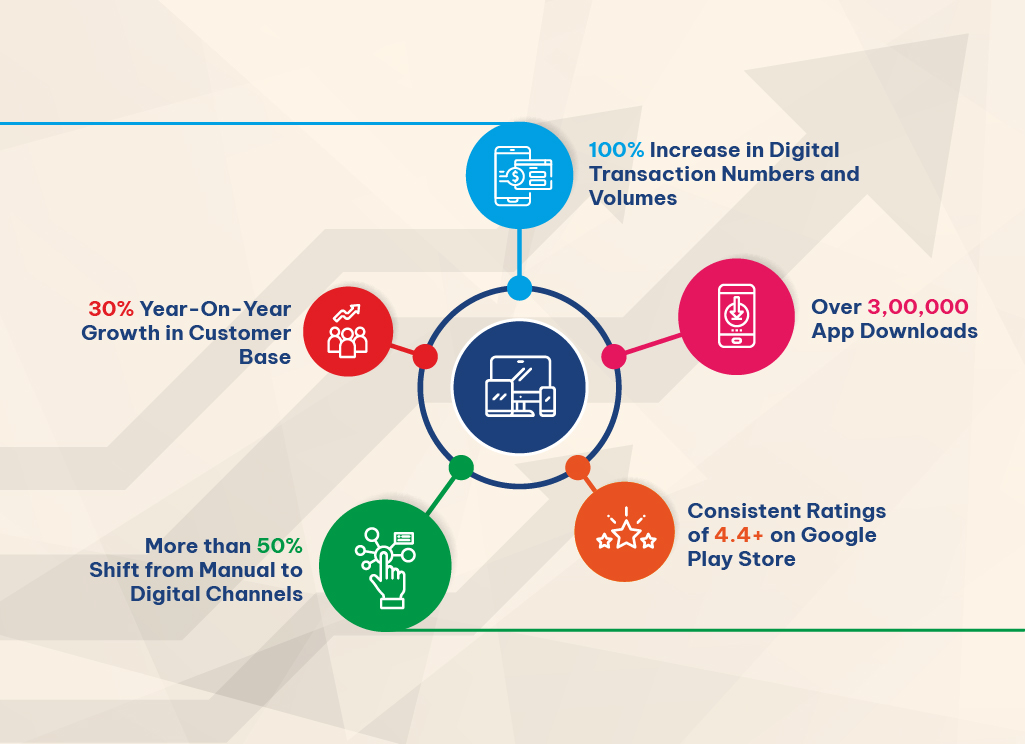

Real-World Example: The BRAC Bank Case

Let’s take a closer look at an example of how digital banking is evolving in Bangladesh – the partnership between Clayfin and BRAC Bank.

Focused on digitising its offerings across retail, SME, and wholesale banking, the bank sought to enhance its infrastructure to meet rising customer expectations. Clayfin worked with BRAC Bank to design and implement a cutting-edge digital platform.

This collaboration yielded impressive results: